Whether you’re buying a house among the Fort Lauderdale homes for sale or any other destination, it’s important to understand mortgage interest rates. Mortgage rates have continued to increase in 2018, and according to Bankrate and most experts, they’re expected top 5 percent by 2019 with home prices continuing to rise.

How Mortgage Interest Rates are Decided

Mortgage interest rates are linked to deposit rates, with the volume of a bank or other lender’s customer deposits and the cost of securing them an essential part of determining what they can afford to lend for home loans. The lender has to source money internationally in order to fund lending demands, with the cost of the funds continuously changing due to global economic conditions and geopolitical events across the globe. For example, during the 2007-2008 global financial crisis, the number of funds that were available dwindled dramatically, and what was available was very costly.

While the Federal Reserve Bank (FED) does not determine mortgage interest rates for conventional loans, adjustable rate mortgages (ARM) and short-term mortgages react to actions taken by the FED. Conventional loans, like 15- or 30-year loans are based on the bond market. Bond investors look at the Fed’s moves resulting in interest rates on long-term bonds going up or down. Even with the Fed shifting short-term rates, rates for longer-term mortgage loans can fluctuate depending on what’s happening in the bond market.

What You Can Do to Get the Lowest Interest Rate

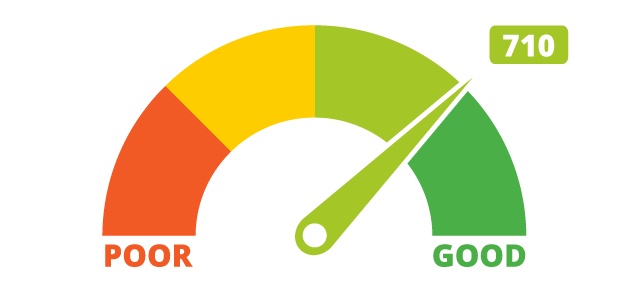

Of course, a potential home buyer has no control over the economy and its ups and downs, the bond market or the Fed, but they do have control of other factors. The loan amount, down payment and credit score, also make a significant difference in determining one’s mortgage interest rate.

To get the best interest rate possible when applying for a mortgage, the higher your credit score the better. Obtain a copy for your credit report from all three credit bureaus: Experian, Transunion, and Equifax. Review these reports thoroughly for any errors and clear them up before completing a home loan application. If there are legitimate issues such as late payments over the last 12 months, be sure that all your payments are made on time and wait another year to improve your score before applying. You’ll also want to pay down any outstanding debt as quickly as you can, as the more debt you have the higher your interest rate will be, or it could keep you from qualifying at all. Lenders will look at the amount of debt you have versus your income, and the lower the ratio, the better.

The amount of money you’ll need to borrow to buy and close on the home impact the mortgage interest rate too. By increasing the amount of your down payment, it reduces the amount you’ll have to borrow and lower the interest rate.

Get Advice From the Experts

Talk to a loan officer to get advice as to what type of mortgage programs may be available to you and ask them what you can do to get the lowest interest rate possible for your situation before applying for a mortgage. Not only will you have a better chance of paying a lower interest rate, but you’ll also be better able to plan, budgeting accordingly.

*This is a sponsored post.

Read more

- You Have to Remember – 9/11, 20 Years Later - September 11, 2021

- Creating the Perfect Look with a Maxi Dress - October 20, 2020

- Brand Better Giveaway - October 6, 2020

Leave a Reply